Two Countries Dominate 80% of the World's Soybean Exports

A highly concentrated global supply chain leaves the world's food and feed systems vulnerable to disruptions in just three countries.

In the study of global logistics and economics, a resilient supply chain is typically defined by diversification. When a critical commodity is produced by dozens of nations and consumed by dozens of others, localized disruptions—such as droughts, political instability, or infrastructure failures—have a muted impact on the global market. However, the global soybean trade operates on the exact opposite principle. Rather than a distributed network, the international soybean market has contracted into a highly concentrated chokepoint.

Today, the global soybean supply chain is dominated by just two primary producers feeding a single, overwhelmingly dominant buyer. If any disruption occurs within this fragile triangle of the United States, Brazil, or China, the shockwaves are felt immediately across the entire global food and feed system.

The Supply Side: A South and North American Duopoly

To understand the scale of this concentration, one must look at global production figures. In 2023, global soybean output reached 390 million tonnes. While soybeans can be grown in various climates, the vast majority of this agricultural output is concentrated in just two nations: Brazil and the United States.

In 2023, Brazil produced around 155 million metric tons of soybeans, establishing itself as the world's leading producer. The United States followed as the second-largest producer, yielding roughly 121 million metric tons of soybeans in the same year. Together, these two nations account for the vast majority of global production, but their dominance is even more pronounced when looking at international trade.

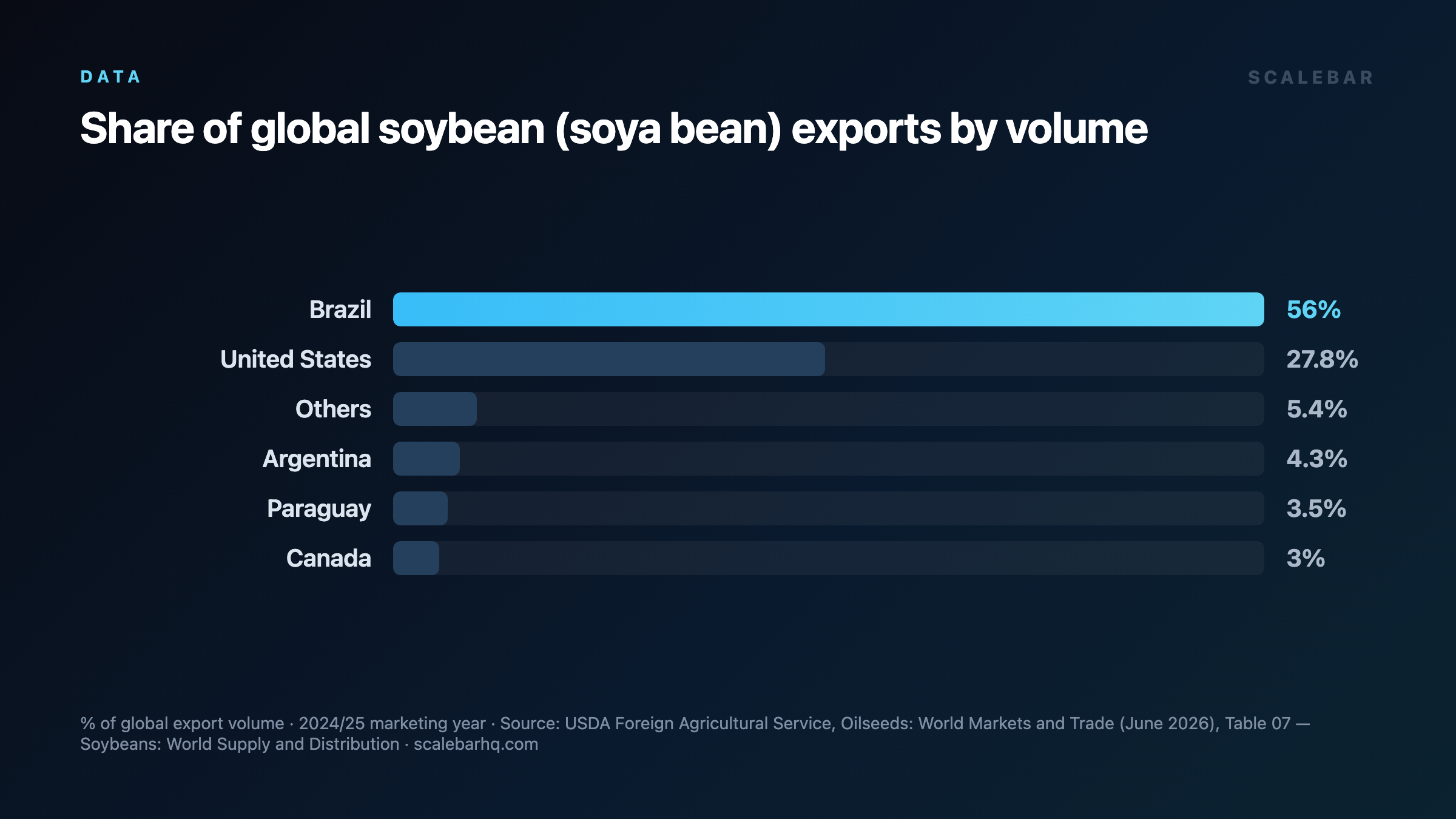

When soybeans cross international borders, the market narrows significantly. Two countries handle over 80% of the world's soybean exports. Brazil alone accounts for 58% of global soybean exports, while the United States accounts for roughly 23%. For any other country attempting to source soybeans on the global market, there are virtually no alternative suppliers capable of operating at this scale.

The domestic infrastructure required to support this level of export volume is staggering. In the United States, the soybean crop during the 2022 to 2023 season was valued at about 60 billion dollars. This massive agricultural endeavor covered roughly 84 million harvested acres across the country. This footprint underscores how deeply integrated soybean cultivation is within the American agricultural economy, yet even this massive output has been surpassed by Brazil's rapid agricultural expansion.

The Demand Side: China's Monopsony Power

While the supply side of the soybean market is controlled by a duopoly, the demand side is characterized by an equally extreme concentration. China has emerged as the ultimate destination for the world's soybean exports, importing over 60% of all soybeans traded globally. No other country comes close to matching this level of consumption.

China's appetite for soybeans has undergone an extraordinary transformation over the last two decades. In 2000, China imported about 12 million tons of soybeans. As the country's economy grew and dietary habits shifted, its reliance on imported protein and oilseeds surged. By around 2010, China's annual soybean imports had risen to roughly 57 million tons.

The upward trajectory continued unabated. By 2017, China imported 93 million tons of soybeans (with some trade records registering about 95 million tonnes). By 2024, this figure had climbed even higher, with China importing close to 100 million tons—and by some measures, more than 105 million tons of soybeans. This represents a nearly tenfold increase in import volume in roughly two decades.

The Vulnerability of a Three-Player System

This extreme concentration of supply and demand creates a highly volatile economic dynamic. Because China relies so heavily on imports to sustain its domestic needs, and because Brazil and the United States are the only nations capable of meeting this demand, the global soybean market is highly sensitive to any disruption.

A severe drought in South America, infrastructure bottlenecks at U.S. ports, or shifts in trade policies between Washington and Beijing can instantly destabilize the market. Because soybeans are a foundational component of the global food and feed system, price fluctuations or supply shortages do not remain confined to the agricultural sector. They quickly cascade into broader food security challenges worldwide.

Ultimately, the global soybean trade is not a highly diversified, resilient market. It is a tightly wound chokepoint where the agricultural policies, weather patterns, and economic health of just three nations dictate the stability of a vital global resource.

Frequently asked

- Which countries dominate global soybean exports?

- The global soybean export market is dominated by Brazil and the United States. Together, these two countries handle over 80% of the world's soybean exports, with Brazil accounting for 58% of global exports and the United States accounting for roughly 23%.

- How much of the global soybean supply does China import?

- China imports over 60% of all soybeans traded globally. Its annual imports have grown from about 12 million tons in 2000 to roughly 57 million tons in 2010, reaching 93 million tons (about 95 million tonnes) in 2017, and climbing to close to 100 million tons (and more than 105 million tons) by 2024.

- What is the scale of soybean production in the United States and Brazil?

- In 2023, global soybean output reached 390 million tonnes. Brazil led production with around 155 million metric tons, while the United States produced roughly 121 million metric tons. In the 2022 to 2023 season, the U.S. soybean crop alone was valued at about 60 billion dollars and covered roughly 84 million harvested acres.

Sources

- https://williams.com.br/usda-brazilian-soy-production-expected-to-reach-169-million-tons

- http://www.ers.usda.gov/data-products/charts-of-note/87915

- https://southernagtoday.org/2024/10/02/brazil-expected-to-continue-dominance-of-global-soybean-exports/

- https://www.iowafarmbureau.com/Article/South-American-Soybean-Production-Update

- https://farmdocdaily.illinois.edu/2024/02/the-united-states-brazil-and-china-soybean-triangle-a-20-year-analysis

- https://www.facebook.com/AmericanSoybeanAssociation/posts/china-bought-52-of-our-soybean-exports-in-2024-said-american-soybean-association-1087081123460068/

- https://www.spglobal.com/energy/en/news-research/latest-news/agriculture/032526-brazil-sets-new-records-as-global-soybean-leader-amid-us-china-trade-tensions

- https://www.reddit.com/r/farming/comments/1jfppv0/chinas_soybean_imports_from_us_jump_84_in_first/

- https://www.sciencedirect.com/science/article/pii/S2666675825003273

- https://www.sei.org/features/brazilian-soy-exports-and-deforestation/

- https://farmdocdaily.illinois.edu/2024/02/the-united-states-brazil-and-china-soybean-triangle-a-20-year-analysis.html

- https://www.researchgate.net/publication/386020271_Analysis_of_world_trends_in_soybean_production

- http://www.brazilintl.com/crops-soybeans.html

- https://www.marketdataforecast.com/market-reports/soybean-market

- https://www.tendata.com/blogs/export/6488.html

- https://farmdocdaily.illinois.edu/2025/12/can-china-reduce-soybean-import-demand-evaluating-soybean-meal-reduction-efforts.html

- https://unitedsoybean.org/hopper/total-u-s-soy-exports-add-39-8-billion-to-u-s-economy-in-marketing-year-22-23

- https://www.statista.com/statistics/863112/soybean-import-volume-to-china/

- https://www.brownfieldagnews.com/news/2024-u-s-soybean-production-tops-2023

- https://www.statista.com/statistics/777211/brazil-soybean-production/

- https://www.facebook.com/AgDay/posts/chinas-soybean-imports-reached-a-record-high-in-august-2024-reflecting-significa/1067982225328991

- http://dimsums.blogspot.com/2025/01/chinas-2024-ag-imports-shrank-in-value.html

- https://www.facebook.com/dtnprogressivefarmer/posts/china-will-import-349-billion-bushels-of-soybeans-in-201718-crop-year-then-keep-/10155225747059069

- https://soygrowers.com/wp-content/uploads/2024/06/24ASA-001-Soy-Stats-Web.pdf