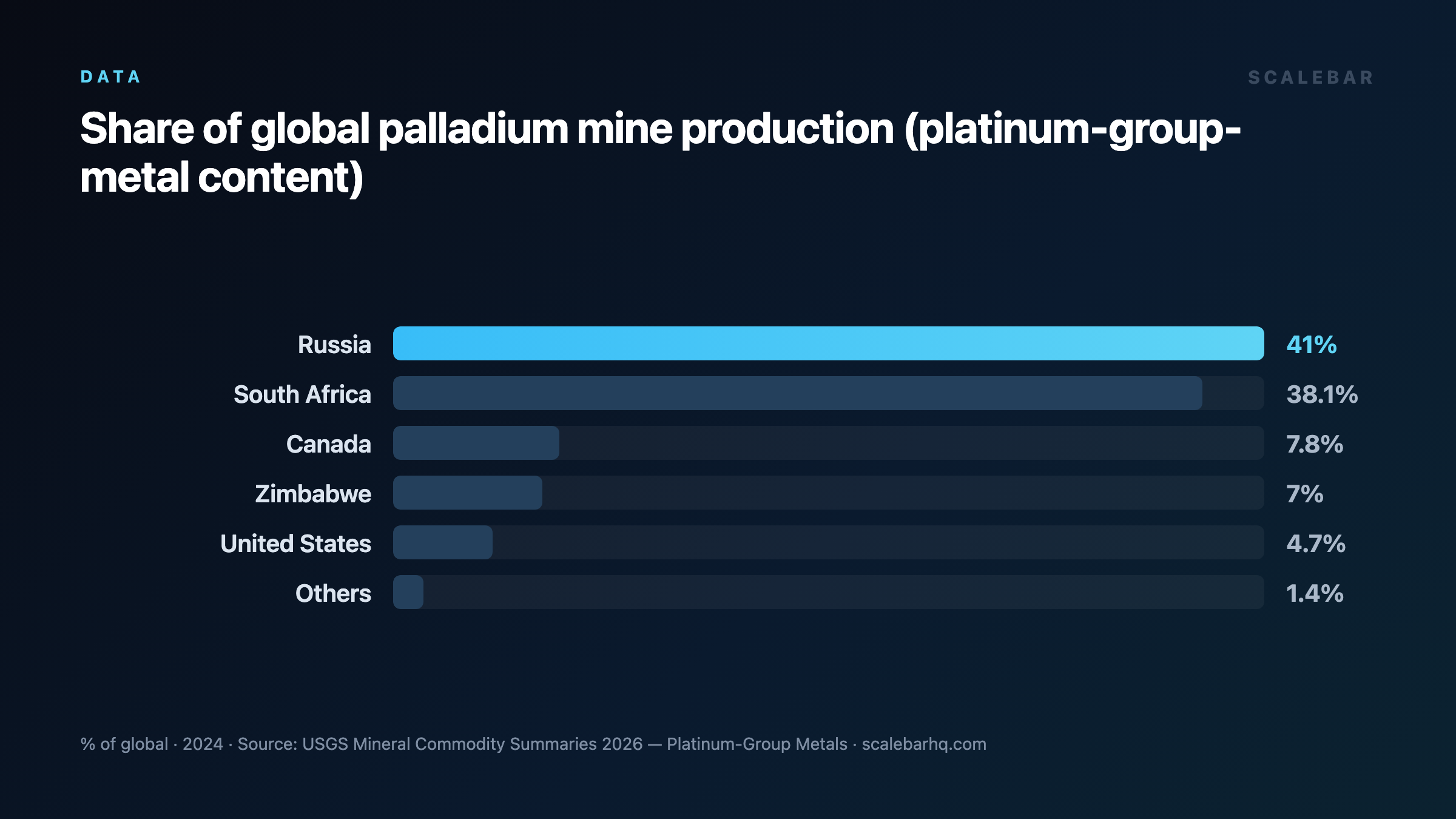

One Country Produces 40 Percent of the World's Palladium

With 40 percent of global supply originating from a single Siberian complex, palladium represents one of the most concentrated critical mineral vulnerabilities on Earth.

In the global conversation surrounding critical minerals and the transition to cleaner transportation, public attention remains largely fixed on battery metals like lithium, cobalt, and nickel. Yet, a far more concentrated and geopolitically sensitive metal quietly underpins the global automotive industry: palladium. This rare, silvery-white platinum group metal is a fundamental component in modern environmental regulation. Without it, contemporary vehicle emissions standards would simply collapse.

Palladium's primary utility lies in its catalytic properties. Inside almost every gasoline-powered and hybrid vehicle on the planet, palladium works within catalytic converters to scrub toxic exhaust gases before they exit the tailpipe. Because of this, the automotive sector is the overwhelming driver of global demand for the metal, consuming approximately 80 percent of all palladium produced worldwide. Within this automotive segment, 80 percent or more of the palladium used is directed specifically toward gasoline catalytic converters. While other industries utilize the metal—most notably dentistry, which accounts for 8 percent of global palladium demand—the fortunes of the palladium market are inextricably linked to the global automotive supply chain.

The Extreme Concentration of Global Supply

What makes palladium uniquely vulnerable to geopolitical disruption is the extreme geographic concentration of its extraction. Unlike copper or iron, which are mined across dozens of jurisdictions globally, the palladium supply chain is dominated by just two nations: Russia and South Africa.

Russia stands as the world's leading producer, mining roughly 40 percent of all palladium globally. Remarkably, this massive share is not distributed across a vast network of domestic mines. Instead, most of Russia's palladium originates from a single, highly remote industrial complex located in Norilsk, deep within Siberia. This extreme concentration of production in a single geographic point makes the global supply chain exceptionally fragile.

South Africa serves as the primary alternative to Russian supply, producing roughly 35 percent of the world's palladium. However, South Africa's mining sector is plagued by systemic vulnerabilities. The country's mines face chronic power cuts and are burdened by aging infrastructure, keeping global supply tight and limiting South Africa's ability to rapidly scale up production during global supply disruptions.

Beyond these two dominant players, global production drops off precipitously. Canada produces roughly 8 percent of global palladium, while Zimbabwe accounts for approximately 7 percent. While these nations contribute to the global market, their relatively small market shares mean they lack the capacity to offset a major disruption from either Russia or South Africa.

Geopolitical Shocks and Price Volatility

The extreme concentration of palladium mining has historically translated into severe market volatility, with prices reacting sharply to geopolitical tensions and supply anxieties.

In 2019, the price of palladium per ounce stood at $1519 USD. As industrial demand surged and supply remained tight, the price climbed dramatically, reaching $2400 USD per ounce in 2021. The onset of the geopolitical crisis in 2022, marked by Russia's invasion of Ukraine, sent shockwaves through the automotive supply chain. Western automakers, suddenly aware of their deep exposure to Russian mineral exports, scrambled to secure alternative sources. During this period of intense anxiety, the price of palladium remained highly elevated, averaging $2100 USD per ounce in 2022.

However, commodity markets are cyclical, and the scramble to find alternatives, combined with broader macroeconomic shifts, eventually led to a sharp correction. By 2024, the price of palladium per ounce had fallen to $1000 USD. Despite this price decline, the underlying structural vulnerability of the supply chain remains unchanged. A single geopolitical shock or operational disruption at the Norilsk complex in Siberia can instantly ripple straight to the factory floors of global automakers.

The High Cost of Substitution

Faced with the risks of relying on Russian exports, Western automotive manufacturers have actively sought ways to design palladium out of their supply chains. The most obvious candidate for substitution is platinum, another platinum group metal with similar catalytic properties.

However, substituting palladium with platinum is far from a straightforward process. Retooling an entire automotive supply chain—which involves redesigning catalytic converters, testing new formulations, and certifying vehicles to meet strict national emissions standards—is an incredibly slow and expensive endeavor. Retooling an entire auto supply chain takes years, rather than months, to execute at scale.

Consequently, despite the intense desire of Western automakers to reduce their exposure to Russian palladium since 2022, the transition has been slow to materialize. The high cost of retooling, combined with the infrastructure challenges facing South Africa's mining sector, means that Russia's grip on the palladium market remains a critical, unresolved vulnerability for the global automotive industry.

Frequently asked

- Which country produces the most palladium?

- Russia is the world's leading producer, mining roughly 40% of all palladium globally. Most of this production comes from a single complex in Norilsk, Siberia.

- What are the primary uses of palladium?

- The automotive industry is the primary consumer, accounting for around 80% of global palladium demand, with 80% or more of that automotive supply going into gasoline catalytic converters. Dentistry is another notable consumer, accounting for 8% of global demand.

- What other countries produce palladium besides Russia?

- South Africa is the second-largest producer, accounting for roughly 35% of global production. Canada produces roughly 8%, and Zimbabwe produces roughly 7%.

- How has the price of palladium changed in recent years?

- The price of palladium per ounce was $1519 USD in 2019, rose to $2400 USD in 2021, sat at $2100 USD in 2022, and declined to $1000 USD in 2024.

Sources

- https://ipa-news.com/index/about-pgms/pgm-uses/automotive/catalytic-converters.html

- https://www.mining-technology.com/projects/norilsk

- https://www.chards.co.uk/guides/highest-palladium-price-history/755

- https://www.emerald.com/insight/content/doi/10.1108/oxan-db269952

- https://www.bullionbypost.co.uk/palladium-price/20-year-palladium-price-history-dollars-ounce

- https://www.monex.com/palladium-price-outlook-january-2024

- https://www.cmegroup.com/articles/2024/why-palladium-matters-to-the-growth-of-the-platinum-market.html

- https://worldpopulationreview.com/country-rankings/palladium-production-by-country

- https://theoregongroup.substack.com/p/palladium-market-confronts-deficits

- https://www.phoenixrefining.com/blog/russia-s-role-in-the-palladium-market

- https://www.statista.com/statistics/270277/mining-of-rare-earths-by-country/

- https://ipa-news.com/index/sustainability/social

- https://english.ckgsb.edu.cn/knowledge/article/china-dominance-of-rare-earth-and-impact-on-global-market/

- https://investingnews.com/palladium-outlook-2021

- https://pmrcc.com/en/news-blog/platinum-group-metals-(pgms)/palladium-in-catalytic-converters

- https://platinuminvestment.com/files/843744/WPIC_Platinum_Essentials_May_2024.pdf

- https://www.facebook.com/scmp/posts/china-currently-accounts-for-about-70-per-cent-of-global-rare-earth-mining-and-p/1395445202631528/

- https://en.wikipedia.org/wiki/List_of_countries_by_palladium_production

- https://www.worldpopulationreview.com/mining/countries-producing-palladium

- https://corarefining.com/good-time-sell-palladium-dental-scrap

- https://grokipedia.com/page/List_of_countries_by_palladium_production