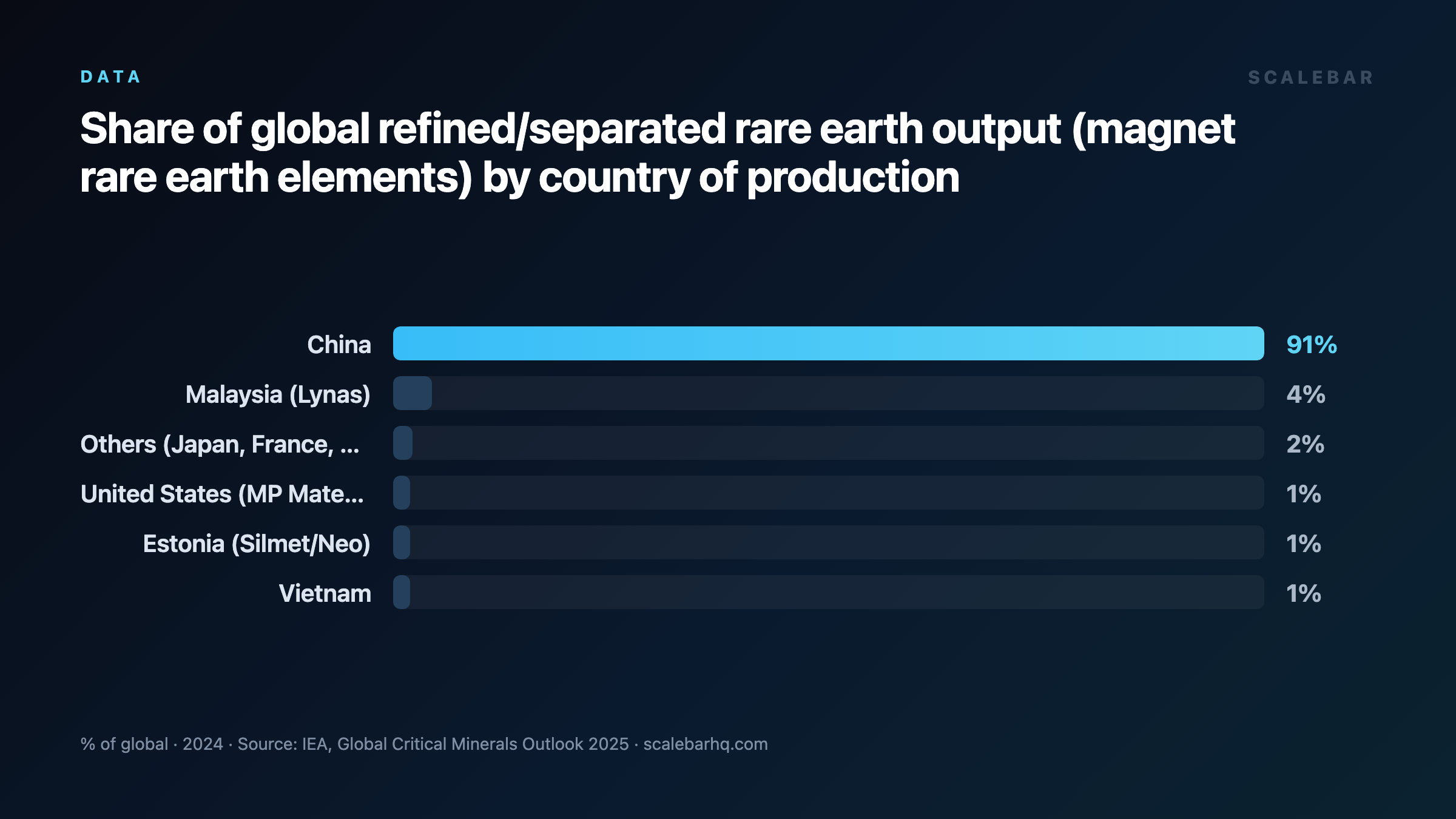

One Country Controls 85% of Rare Earth Processing

While multiple nations extract these 17 critical metals, China's near-monopoly on the refining process creates a massive global supply chain bottleneck.

The modern global economy relies on a highly complex and deeply integrated network of supply chains, but few are as concentrated—or as geopolitically sensitive—as the market for rare earth elements. These materials are the invisible backbone of twenty-first-century technology. They are found inside the smartphones in our pockets, the batteries powering the transition to electric vehicles, the wind turbines generating renewable energy, and the guidance systems of advanced military fighter jets. Without them, the production of modern technology would grind to a halt.

While many associate resource dominance with geological abundance, the true story of rare earths is not merely about who has these minerals in the ground. Instead, it is a story of industrial processing capacity. Today, one country controls the vast majority of this supply chain, not just by extracting the raw materials, but by dominating the highly complex chemical refining processes required to make them usable. That country is China.

What Are Rare Earths?

Despite their name, rare earth elements are not particularly rare in the Earth's crust. They are, however, difficult to find in concentrations that are economically viable to mine, and even more difficult to separate and purify. Globally defined as a group of 17 metals, these elements possess unique magnetic, luminescent, and electrochemical properties that make them irreplaceable in high-tech manufacturing.

Because these 17 metals are chemically similar, they are almost always found mingled together in nature. Separating them into high-purity, individual elements requires highly advanced, multi-stage chemical engineering. This industrial complexity is the primary reason why the rare earth supply chain is so vulnerable to disruption.

Mining vs. Refining: The Real Bottleneck

To understand China's dominance, it is necessary to separate the supply chain into two distinct phases: extraction (mining) and processing (refining).

In the extraction phase, China is already the undisputed leader, mining around 70% of all rare earths extracted globally each year. No other country comes close to this level of output. However, mining is only the first step. Raw, unrefined ore is virtually useless to manufacturers of electric vehicles or consumer electronics.

To become usable components, the mined ore must undergo a highly sophisticated refining process. This is where the bottleneck tightens significantly. China refines roughly 85% of all rare earths worldwide. This means that even when other nations successfully extract rare earth minerals from their own soil, they remain almost entirely dependent on Chinese infrastructure to turn those minerals into finished, industrial-grade materials.

The United States and the Processing Paradox

This reliance on Chinese refining capacity has created a stark geopolitical paradox, particularly for the United States. Decades ago, the United States led the global rare earth industry, possessing both the mining and refining capabilities necessary to meet domestic demand. Over time, however, domestic processing capacity declined, and production shifted overseas.

Today, the United States still mines rare earth minerals domestically, but it lacks the industrial infrastructure to process them. As a result, the U.S. ships most of its mined ore across the Pacific to China for processing. Once Chinese facilities refine the raw ore into usable metals and magnets, the United States buys it back as finished product. This circular supply chain highlights how geological reserves mean very little without the domestic capacity to refine them.

The High Barriers to Diversification

As geopolitical tensions rise and the risks of supply chain concentration become more apparent, Western nations are eager to diversify their sources. Countries like Australia, Canada, and Brazil hold significant geological reserves of rare earths, offering a potential alternative to Chinese extraction.

However, translating these reserves into a functioning, independent supply chain is an incredibly slow and expensive endeavor. Building a single rare earth refinery is not a matter of months, but of years. Industry estimates indicate that establishing a fully operational refinery takes a decade and requires billions of dollars in capital investment.

For private companies and governments, this represents a massive financial and operational hurdle. Beyond the sheer cost, building these facilities requires navigating complex environmental regulations, securing specialized chemical engineering expertise, and competing against established Chinese processors that benefit from decades of scale and state support.

A Looming Demand Spike

The urgency to build alternative refining capacity is compounded by a massive projected increase in global demand. Driven almost entirely by the global transition toward clean energy technologies—specifically the manufacturing of electric vehicle (EV) motors and wind turbines—the demand for rare earths is expected to triple by 2040.

With demand poised to skyrocket, the existing supply chain bottleneck is expected to get even tighter. The United States, the European Union, and Australia are currently engaged in a rapid race to fund and construct domestic refining facilities. Governments are offering subsidies and forming strategic alliances to secure their technological futures.

Yet, because of the decade-long timeline required to build these refineries, these initiatives will take years to bear fruit. For the foreseeable future, the global transition to green energy and the production of advanced electronics will remain heavily reliant on the processing facilities of a single nation.

Frequently asked

- What are rare earths and why are they important?

- Rare earths are a group of 17 metals that are essential for manufacturing modern technologies, including smartphones, electric vehicle batteries, wind turbines, and military fighter jets.

- How much of the global rare earth market does China control?

- China mines around 70% of all rare earths extracted globally each year and refines approximately 85% of the world's supply, giving it near-total control over the processing stage of the supply chain.

- Why does the United States ship its rare earth ore to China?

- Although the United States mines rare earth ore domestically, it lacks the necessary refining infrastructure to process it. Consequently, the U.S. ships most of its mined ore to China for processing and then buys it back as finished product.

- Why is it difficult for other countries to build their own rare earth refineries?

- Building a rare earth refinery is highly capital-intensive and time-consuming. It typically takes a decade and billions of dollars to construct and commission a single processing facility.

Sources

- https://worldpopulationreview.com/country-rankings/rare-earth-reserves-by-country

- https://elements.visualcapitalist.com/charted-where-the-u-s-gets-its-rare-earths-from/

- https://en.wikipedia.org/wiki/Rare-earth_industry_in_Australia

- https://pubs.usgs.gov/periodicals/mcs2024/mcs2024-rare-earths.pdf

- https://unece.org/sites/default/files/2025-03/02.%20Tae-Yoon_Kim.pdf

- https://investingnews.com/pentagon-funds-rare-earth-refining/

- https://investingnews.com/daily/resource-investing/critical-metals-investing/rare-earth-investing/rare-earth-reserves-country/

- https://en.wikipedia.org/wiki/Rare-earth_element

- https://www.usitc.gov/publications/332/executive_briefings/ebot_rare_earths_part_1.pdf

- https://www.statista.com/statistics/270277/mining-of-rare-earths-by-country/

- https://www.ga.gov.au/aimr2024/world-rankings

- https://www.csis.org/analysis/developing-rare-earth-processing-hubs-analytical-approach

- https://www.facebook.com/scmp/posts/china-currently-accounts-for-about-70-per-cent-of-global-rare-earth-mining-and-p/1395445202631528/

- https://en.wikipedia.org/wiki/Rare-earth_industry_in_China

- https://pubs.usgs.gov/periodicals/mcs2025/mcs2025-rare-earths.pdf

- https://x.com/IGWTreport/status/1978415824600748048

- https://www.facebook.com/groups/229881329205/posts/10164614393769206/

- https://www.statista.com/statistics/270277/mining-of-rare-earths-by-country

- https://iea.blob.core.windows.net/assets/ffd2a83b-8c30-4e9d-980a-52b6d9a86fdc/TheRoleofCriticalMineralsinCleanEnergyTransitions.pdf

- https://www.facebook.com/groups/229881329205/posts/10164614393769206

- https://finance.yahoo.com/markets/commodities/articles/china-controls-90-rare-earth-090000286.html

- https://www.china-briefing.com/news/chinas-rare-earth-elements-dominance-in-global-supply-chains/

- https://www.mining-technology.com/analyst-comment/china-global-rare-earth-production/

- https://ejatlas.org/print/rare-earth-mining-in-mountains-of-myanmar