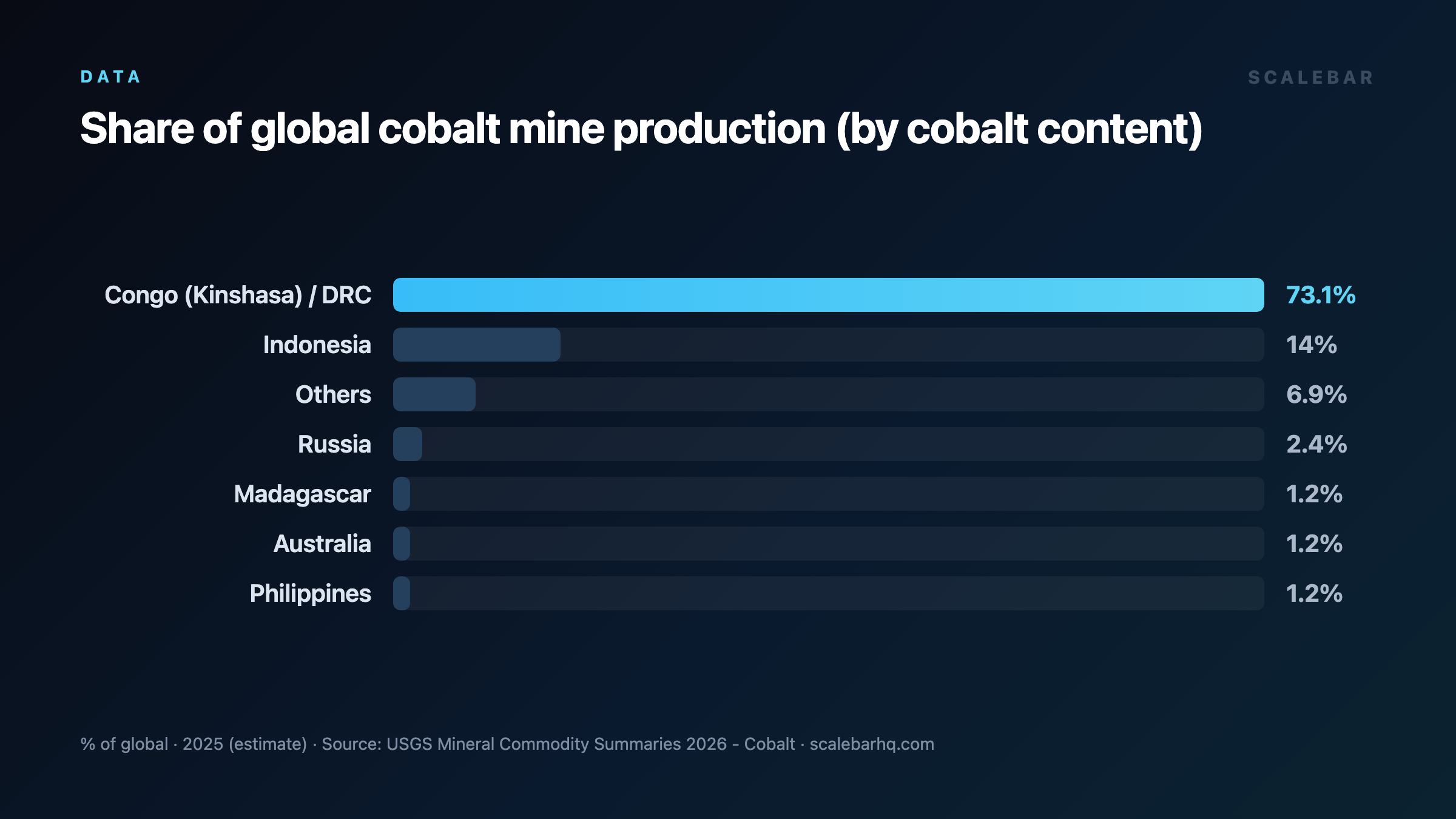

One Country Controls 70% of the World's Cobalt

How a bilateral pipeline between the DRC and China holds the key to the global electric vehicle transition.

The global transition toward clean energy and mobile technology relies on a complex network of supply chains, but none is as highly concentrated—or as vulnerable—as the supply chain for cobalt. Essential for the production of high-energy-density lithium-ion batteries, cobalt is the quiet engine behind the electric vehicle (EV) revolution and the proliferation of modern smartphones. Yet, the global supply of this critical mineral does not flow from a diverse array of international producers. Instead, the entire system hinges on a single geographic bottleneck: the Democratic Republic of Congo (DRC).

The DRC's near-monopoly on cobalt extraction makes it the single most critical chokepoint in the global battery supply chain. As nations scramble to secure their energy futures, understanding the dynamics of this pipeline—from the mines of the DRC to the processing facilities of China—is essential to understanding the geopolitics of the twenty-first century.

The Extraction Giant

At the heart of the global battery industry lies a stark geographic reality: the Democratic Republic of Congo produces roughly 70% of global cobalt. This overwhelming share of production places the DRC in a position of unprecedented leverage over the global tech and automotive sectors. Without cobalt, manufacturing the lithium-ion batteries that power consumer electronics and electric vehicles is currently unfeasible at scale.

While other nations possess cobalt reserves, their output is negligible by comparison. Other producing nations, such as Russia and Australia, lag far behind, contributing only minor fractions to the global supply. This extreme concentration of a vital resource in a single country creates a highly sensitive supply chain. Any localized disruption within the DRC—whether caused by political instability, labor disputes, infrastructure deficits, or regulatory changes—has the potential to trigger immediate shortages and price spikes worldwide, directly impacting automotive factories and electronics manufacturers across the globe.

The Refining Bottleneck

While the DRC dominates the extraction of raw cobalt, it possesses very little domestic refining capacity. The raw ore extracted from Congolese mines cannot be directly integrated into battery cells; it must first undergo a highly specialized chemical refining process to reach the purity levels required for battery chemistry.

This is where the second major node of the global chokepoint emerges. About 80% of raw cobalt extracted from the DRC is shipped directly to China for processing. China has systematically built a dominant position in the midstream of the battery supply chain, establishing the vast majority of the world's refining capacity.

Consequently, the journey of a single cobalt atom typically follows a highly centralized path: it is mined in the DRC, shipped across the ocean to Chinese refineries, processed into battery-grade chemicals, and then integrated into battery cells that are distributed to global markets. This structure means that the global battery supply chain is not merely dependent on one country, but rather on a bilateral pipeline running from the DRC to China. Even if alternative mining sources were to emerge, the global industry would still remain heavily reliant on Chinese refining infrastructure to process the raw material.

Geopolitical and Economic Implications

This concentrated supply chain presents significant strategic challenges for global automakers and Western governments. The reliance on a DRC-to-China pipeline exposes the global transition to clean energy to severe geopolitical risks. Trade tensions, export controls, or logistical disruptions at any point along this route could stall the production of electric vehicles globally.

For automakers, this vulnerability has transformed supply chain management from a logistical detail into a matter of corporate survival. The realization that the entire electric vehicle revolution runs through a single, economically fragile nation has forced a reevaluation of manufacturing strategies. Companies are increasingly seeking ways to bypass this chokepoint, investing heavily in research and development to find alternative battery chemistries.

The Search for Alternatives

In response to the risks associated with the cobalt supply chain, the battery industry is actively exploring cobalt-free alternatives. Technologies such as Lithium Iron Phosphate (LFP) batteries, which do not require cobalt, have gained traction, particularly for entry-level electric vehicles and stationary energy storage. Other experimental chemistries are also being researched in hopes of completely eliminating the mineral from high-performance batteries.

However, transitioning away from cobalt is a slow and technically challenging process. Cobalt plays a crucial role in stabilizing battery chemistry and maintaining high energy density, which directly translates to longer driving ranges for electric vehicles. For high-performance applications, cobalt remains difficult to replace. As a result, even as alternative chemistries emerge, global demand for cobalt is projected to grow significantly as the adoption of electric vehicles accelerates worldwide. This growing demand is expected to tighten the existing chokepoint, making the DRC's role in the global economy even more pivotal in the coming years.

Conclusion

The transition to a decarbonized economy is often framed as a shift away from resource dependency, but in reality, it replaces a dependency on fossil fuels with a dependency on critical minerals. The cobalt supply chain is the most extreme example of this new paradigm. With the DRC producing roughly 70% of global cobalt and China processing about 80% of that raw material, the path to a clean energy future remains remarkably narrow. Until viable, scalable alternatives are fully realized, the global battery supply chain will continue to run through this critical geopolitical bottleneck.

Frequently asked

- What percentage of the world's cobalt is produced by the Democratic Republic of Congo?

- The Democratic Republic of Congo (DRC) produces roughly 70% of the global cobalt supply, making it the dominant source of this critical battery mineral.

- Where is the majority of the raw cobalt mined in the DRC sent for processing?

- About 80% of the raw cobalt extracted from the DRC is shipped directly to China for refining and processing before it enters the global battery supply chain.

- Why is the cobalt supply chain considered a major global chokepoint?

- The supply chain is highly concentrated at two key stages: roughly 70% of extraction occurs in a single country (the DRC), and about 80% of that raw material is processed in another single country (China). This extreme geographic concentration makes the entire global battery and electric vehicle industry highly vulnerable to localized disruptions.

Sources

- https://www.mining-technology.com/data-insights/cobalt-in-australia/

- https://mst.misis.ru/jour/article/view/909

- https://metals.co/wp-content/uploads/2023/11/Benchmark_Carbon-Sinks_Summary_2023.pdf

- https://www.evidencity.com/drc

- https://pmc.ncbi.nlm.nih.gov/articles/PMC6166862/

- https://www.statista.com/statistics/339834/mine-production-of-cobalt-in-dr-congo/

- https://www.reuters.com/world/china/global-cobalt-market-seen-swinging-deficit-surplus-early-2030s-2025-05-14/

- https://www.mining-technology.com/data-insights/cobalt-in-the-philippines/

- https://resourcetrade.earth/publications/critical-metals-ev-batteries

- https://www.ga.gov.au/aimr2024/world-rankings

- https://finance.yahoo.com/markets/commodities/articles/democratic-republic-congo-drc-cobalt-153800115.html

- https://en.wikipedia.org/wiki/Lithium_batteries_in_China

- https://www.investkorea.org/ik-en/cntnts/i-3025/web.do

- https://www.csis.org/analysis/new-phase-us-battery-industry

- https://globaledge.msu.edu/countries/democratic-republic-of-the-congo/economy

- https://www.cobaltinstitute.org/wp-content/uploads/2025/05/Cobalt-Market-Report-2024.pdf

- https://innovationreform.org/wp-content/uploads/2024/05/2024-05-Korea-Energy-EV-batteries.pdf

- https://www.worldbank.org/ext/en/country/drc

- https://www.mining-technology.com/data-insights/cobalt-in-cuba/

- https://pubs.usgs.gov/periodicals/mcs2024/mcs2024-cobalt.pdf

- https://natural-resources.canada.ca/minerals-mining/mining-data-statistics-analysis/minerals-metals-facts/cobalt-facts

- https://www.facebook.com/TheEIU/posts/china-accounted-for-about-733-of-global-lithium-battery-manufacturing-capacity-a/680828877407561/

- https://pubs.usgs.gov/myb/vol3/2023/myb3-2023-china.pdf

- https://publica.fraunhofer.de/bitstreams/3686ab8b-b174-457e-9237-327b149534c9/download