3 Countries Control Half the World's Copper

The global transition to green energy relies on a copper supply chain dominated by just a few key nations.

Copper is the quiet backbone of the modern world's transition toward a cleaner energy future. It is an indispensable component found in every electric vehicle, every solar panel, and every major electrical grid upgrade. As nations push to decarbonize their economies, the demand for this highly conductive red metal is poised to skyrocket. Projections indicate that global copper demand is forecast to double by 2035. Looking further ahead, by 2050, the world will need roughly 70 percent more copper than it uses today.

However, this massive surge in demand faces a critical bottleneck: the global copper supply chain is highly concentrated in just a few nations. This extreme concentration of both mining and refining capacity leaves the global green energy transition highly vulnerable to geopolitical shocks, trade disputes, and localized disruptions.

The South American Powerhouses

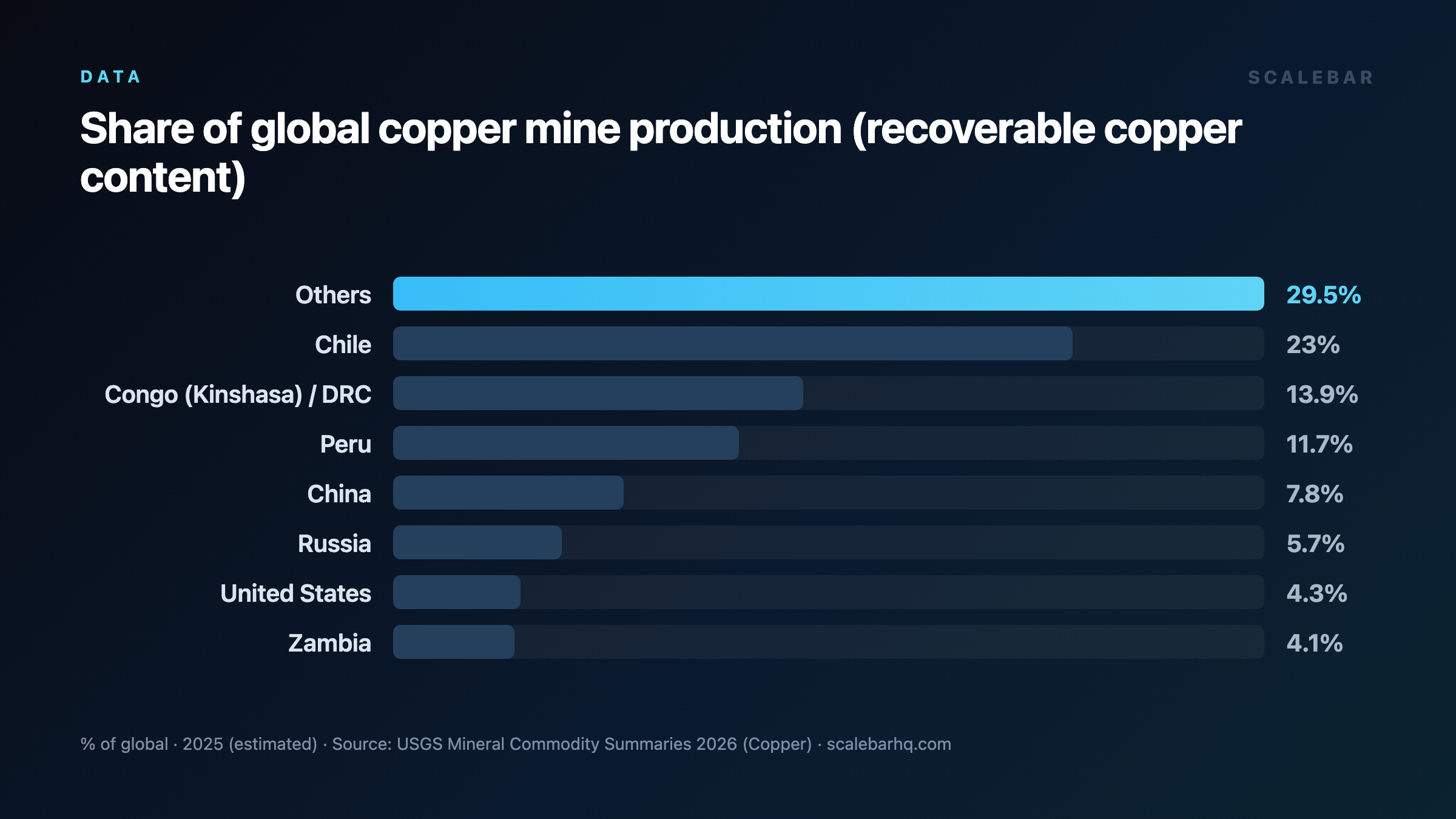

Geologically, copper is not distributed evenly across the globe. A massive portion of the world's copper wealth is concentrated along the Andean mountain range of South American nations. Chile stands as the undisputed titan of the copper mining world. The nation produces about 24 percent of global copper, making it the world's leading producer. Furthermore, Chile sits on the single largest copper reserves of any country on the planet.

But Chile's regional dominance is only part of the story. When combined with its northern neighbor, Peru, the geopolitical weight of South American copper becomes even more pronounced. Together, Chile and Peru hold roughly one third of the world's copper reserves. This means that two neighboring nations sit on one enormous geological jackpot, giving them unprecedented leverage over the raw materials required for global electrification. Any political instability, labor disputes, or environmental policy shifts in these two countries could instantly reverberate through global markets, stalling green energy projects worldwide.

The Rapid Rise of the Democratic Republic of Congo

While South America has historically dominated copper extraction, a new heavyweight has rapidly emerged in Central Africa. The Democratic Republic of Congo (DRC) has experienced an unprecedented mining boom, positioning itself as a critical player in the global supply chain. The DRC is now the number two global copper producer, overtaking other traditional mining powerhouses.

The speed of the DRC's ascent is particularly remarkable. The country's copper output has doubled in under a decade. This rapid expansion has been fueled by massive investments in high-grade deposits, transforming the DRC into the fastest-rising producer on the planet. However, relying on a nation with such rapid growth but complex domestic dynamics adds another layer of risk to the global supply chain.

The Refining Bottleneck: China's Dominance

To understand the true vulnerability of the copper supply chain, one must look beyond where the metal is dug out of the ground. Mining and refining are two very different kinds of power. While countries like Chile and the DRC dominate the extraction of raw copper ore, they do not necessarily turn it into the high-purity, usable metal required for industrial applications.

This is where China plays a dominant role. China barely mines copper at home, possessing relatively limited domestic reserves. Yet, through massive industrial planning and investment in processing infrastructure, China refines nearly 60 percent of the world's copper.

This creates a profound geographical disconnect in the supply chain. Raw copper mined in South America and Africa must be shipped across oceans to Chinese smelters and refineries before it can be used to manufacture electric vehicles, wind turbines, or transmission lines. This extreme concentration of refining capacity gives China immense geopolitical leverage. If trade tensions flare or supply routes are disrupted, the rest of the world could find itself with plenty of raw ore but a severe shortage of the refined copper needed to build green infrastructure.

The Vulnerability of Major Consumers

The geopolitical risks of this concentrated supply chain are acutely felt by major consuming nations, particularly the United States. As the US attempts to rebuild its domestic manufacturing, upgrade its aging electrical grid, and accelerate electric vehicle adoption, its reliance on foreign copper poses a significant strategic challenge.

Currently, the United States imports roughly half the copper it consumes. This high level of import reliance leaves American industries highly exposed to international market fluctuations and supply chain bottlenecks.

Furthermore, the US import profile is highly concentrated. Chile is the biggest copper supplier to the United States. This means that a single trade relationship underpins a vast portion of American grid infrastructure and clean energy manufacturing. Any disruption to this bilateral trade flow—whether due to political shifts in South America, shipping bottlenecks, or trade disputes—could directly threaten the United States' ability to maintain and expand its electrical infrastructure.

With reserves concentrated in the Andes, production surging in the DRC, refining concentrated in China, and major economies like the United States relying heavily on imports, copper has quietly become one of the most strategically critical metals in the world. If the world is to meet its ambitious climate goals for 2035 and 2050, navigating the geopolitical realities of this concentrated supply chain will be just as important as the engineering challenges of the green transition itself.

Frequently asked

- How much is global copper demand expected to grow?

- Copper demand is forecast to double by 2035. By 2050, the world will need roughly 70 percent more copper than it uses today.

- Which countries hold the largest share of the world's copper reserves?

- Chile has the single largest copper reserves of any country. Together, Chile and Peru hold roughly one third of the world's copper reserves.

- How fast is copper production growing in the Democratic Republic of Congo?

- The Democratic Republic of Congo is now the number two global copper producer, and its copper output has doubled in under a decade.

- What role does China play in the copper supply chain?

- While China barely mines copper at home, it refines nearly 60 percent of the world's copper into usable metal.

- How dependent is the United States on copper imports?

- The United States imports roughly half the copper it consumes, and Chile is its biggest copper supplier.

Sources

- https://features.csis.org/copper-in-latin-america

- https://finance.yahoo.com/news/democratic-republic-congo-copper-mining-101500969.html

- https://oilprice.com/Energy/Energy-General/A-Major-Copper-Crunch-Is-Looming.html

- https://www.csis.org/analysis/tariffs-copper-imports-will-affect-45-percent-us-copper-needs

- https://www.developmentaid.org/news-stream/post/186305/top-10-largest-copper-producing-countries

- https://www.facebook.com/businessinsiderssa/posts/top-10-copper-exporting-countries-in-africa1-democratic-republic-of-congo-2-zamb/771997465387200

- https://www.gbreports.com/contents/chilean-copper-production-and-development

- https://www.opportimes.com/en/top-10-copper-exporters-to-the-united-states-in-2024

- https://www.reuters.com/markets/commodities/china-2025-copper-output-set-hit-record-high-despite-feedstock-shortages-2025-08-01

- https://www.riotimesonline.com/drc-congo-retains-second-place-in-global-copper-production-for-2024

- https://www.tomorrowsworldtoday.com/manufacturing/copper-demand-projected-to-double-by-2035

- https://www.vinachem.com.vn/content/market-and-product-vnc/5-top-copper-reserves-by-country.html